Executive Summary: The Commodification of the Atmosphere

I start this investigation with a distinction that often disappears in public debate: a compliance allowance surrendered under a statutory cap is not the same instrument as a voluntary offset used in a corporate marketing claim. Treating them as identical weakens the critique. It lets defenders of carbon markets hide behind technical corrections while the larger financial architecture keeps expanding.

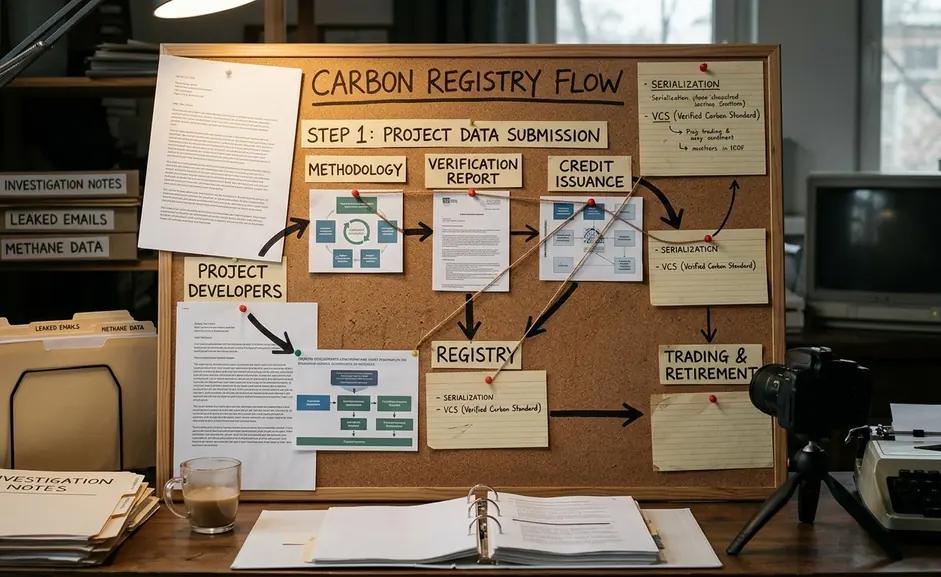

The asset being traded is not the sky. It is a serialized entry in a registry: an allowance or credit with ownership transfers logged before surrender or retirement. Compliance systems generally force covered facilities to monitor emissions, report them to a regulator, undergo verification, and surrender allowances on a fixed annual cycle. Voluntary programs usually issue one credit for one metric tonne of claimed CO₂-equivalent reduction or removal, then mark that credit as retired when a buyer uses it for a claim.

The instrument comes first

The environmental story comes later. That order matters.

- Statutes create allowances inside compliance markets.

- Project documents create the basis for offset issuance.

- Registries turn those claims into tradable records.

- Financial desks, brokers, and corporate buyers give those records market value.

Major compliance-market infrastructure expanded in phases during 2005-2007, 2008-2012, and 2013-2020, per documented metrics. Later rulemaking during 2021-2024 focused on cross-border crediting and registry interoperability. In plain terms, the system matured from a regulatory tool into a financial network.

Summary: Carbon markets do not commodify the atmosphere directly. They commodify permissions, claims, and registry entries tied to atmospheric accounting.

The nuance is important. Some facilities do face real compliance duties. Some projects do produce measurable reductions. But the governing logic remains financial: define a unit, serialize it, transfer it, and settle it. Once that structure exists, the market can grow even when the environmental benefit remains contested.

The Financialization of Nature

Consider the office file behind a single forestry-based offset. It usually contains a baseline scenario, a monitoring plan, third-party validation, periodic verification, issuance into a registry account, and eventual retirement. The forest may be real. The carbon benefit, however, depends on a counterfactual: what would have happened without the project?

That is where nature becomes finance.

From conservation claim to investable unit

The key shift occurred from the late 1990s through the 2005-2012 compliance-market buildout, when emissions reductions became transferable units rather than site-specific regulatory duties only. Environmentalism once centered on direct restraints: protect the river, regulate the smokestack, preserve the habitat. Carbon capitalism changed the unit of action. It made the reduction itself portable.

Figures such as Al Gore and firms such as Generation Investment Management helped popularize the idea that climate risk could be priced, packaged, and directed through investment channels. Reporting confirms that the broader market architecture moved through carbon accounting, registry-issued credits, funds, brokers, and corporate retirement services. The political appeal was obvious: business could claim climate virtue without surrendering the financial grammar of expansion.

Offset categories during 2006-2012 included industrial gas destruction, landfill methane capture, renewable-energy displacement, fuel switching, and forestry-based carbon storage. Each category carried its own measurement problems. Yet one vulnerability sits at the center of the entire model: additionality.

Note: An offset can fail even when the project exists physically. The failure case is a credit issued for an activity that was already legally required, already financed, or not durably monitored.

This is not a minor accounting footnote. It is the fulcrum of the market. If the reduction would have happened under existing law, ordinary business practice, or already-secured financing, then the credit does not offset anything meaningful. It merely gives a buyer a claim.

The implication is severe. A company can keep emitting, buy a credit, retire the registry entry, and advertise a cleaner profile. The system has traded the right to pollute rather than forcing systemic emission cuts at the source.

Wall Street's New Playground: Carbon Derivatives

What did Wall Street see when it looked at carbon?

Not primarily a forest. Not a smokestack. Nor a community living beside an industrial corridor. It saw exposure: price movement, delivery schedules, eligibility rules, contract risk, and a new class of climate-linked paper.

The supply chain moved upstream

From 2007-2010, some large financial institutions expanded carbon-trading desks while also buying or taking stakes in offset project developers and retail offset providers. JPMorgan's aggressive entry into the climate market, associated with Blythe Masters, followed that logic. The bank did not merely want to trade finished credits. It moved toward the machinery that produced them.

The acquisition of ClimateCare and Eco-Securities Group Plc showed why supply-chain control mattered. Offset control can include project sourcing, contract negotiation with project owners, verification coordination, registry issuance, wholesale resale, and retirement services for corporate buyers. Control the pipeline, and you gain leverage over both supply and narrative.

- Project owners need buyers and contract terms.

- Corporate clients need retirement services and reputational cover.

- Trading desks need inventory, timing, and price exposure.

- Registries and regulators determine whether a credit can actually be used.

Carbon forwards and swaps expose buyers to delivery risk, regulatory-eligibility risk, registry risk, counterparty risk, and price volatility between contract signing and credit issuance. These are not incidental hazards. They are the raw material of derivatives trading.

The parallel with credit-default swaps before the 2008 financial crisis is structural, not identical. Both instruments can detach financial exposure from the underlying real-world asset. Carbon credits add another layer: they depend on project monitoring data and acceptance by a registry or regulator. A mortgage either performs or does not. A carbon credit asks the market to trust a measurement chain, a legal eligibility decision, and a counterfactual climate claim.

The partial answer, then, is uncomfortable. Wall Street did not need carbon markets to solve climate change. It needed carbon markets to become complex enough to trade.

The Geoengineering Smokescreen

In July 2012, a private ocean-fertilization operation west of Canada released a reported roughly 100 tonnes of iron-rich material into the ocean. The stated rationale was plankton growth and salmon restoration. The political significance was broader: a private actor attempted physical climate-adjacent intervention at scale, outside the ordinary public consent people expect for environmental manipulation.

That case deserves close attention because it gives the debate a concrete anchor. It is not necessary to begin with speculation about planetary control. Start with the material act: iron-rich material entered the ocean to stimulate biological response.

Weather control is local; carbon finance is legal

Cloud-seeding programs commonly use aircraft, rockets, or ground generators to disperse silver iodide or similar particles into suitable cloud systems. Municipal and regional weather bureaus have used these methods for precipitation management. Rain-enhancement trials in the Gulf region during 2010-2011 involved ionization equipment mounted on towers, though public scientific debate continued over whether observed rainfall could be attributed to the equipment.

Those examples show capability and ambition. They do not, by themselves, prove a unified command system.

A local cloud-seeding permit, an ocean-fertilization experiment, and a carbon tax operate through different legal authorities and evidence chains, so claims about coordination must be proven case by case. This is where disciplined skepticism matters. Documented geoengineering tests do not by themselves prove that climate volatility is being deliberately manufactured to justify carbon taxes; that claim requires evidence of intent, coordination, and measurable causal effect.

Still, the governance question remains legitimate. Weather modification is usually local or regional in claimed scope, while carbon taxation and emissions trading are legal-financial systems tied to measured or estimated greenhouse-gas inventories. The more unstable the climate narrative becomes, the easier it is for mandatory pricing systems to present themselves as emergency infrastructure.

Quick Tip: Separate the physical intervention from the financial policy. Ask who authorized the intervention, who measured the effect, and who benefits from the resulting legal framework.

Even the speculative edge of geoengineering has entered formal scientific discussion. A scientific paper on space-borne mirrors illustrates how climate intervention concepts can migrate from fringe imagination into technical modeling. The existence of a model is not a deployment plan. But it widens the policy imagination, and that widening has consequences.

Agenda 21 and the Push for Global Taxation

The strongest version of the global-taxation argument must begin by separating binding law from planning language. The 1992 UN sustainable-development action plan is a non-binding framework. It does not itself impose taxes, create a world treasury, or directly seize resources.

That fact does not end the inquiry. It sharpens it.

Where the power actually appears

Enforceable power appears in regional statutes, market rules, compliance deadlines, and penalties. A regional aviation emissions rule took effect for flights beginning in January 2012, initially covering flights arriving in or departing from the region. After diplomatic objections, enforcement narrowed. From 2013-2016 and through later extensions, the rule was largely confined to intra-regional flights while international negotiations continued over a global aviation-offset framework.

This is how extra-territorial pressure often works in practice. It rarely arrives as a single world tax stamped with a global seal. It arrives through jurisdictional reach, market access, reporting duties, and the cost of non-compliance.

Agenda 21 matters less as a tax instrument than as a governing vocabulary: sustainability, resource management, land-use planning, and development coordination. Those phrases can support useful conservation. They can also give institutional cover to resource acquisition control when paired with tradable scarcity and financial penalties.

The suppression question becomes especially sharp when compared with practical materials such as industrial hemp. Hemp can be used for fiber, seed oil, building materials, and biocomposites. Its climate benefit, however, depends on cultivation practices, processing energy, transport distance, land-use change, and product substitution. No crop deserves magical treatment.

Yet the contrast remains revealing. True sustainability asks whether production systems can reduce waste, substitute durable materials, and lower dependence on extractive supply chains. Carbon finance asks whether emissions can be measured, priced, traded, and offset. One path changes material life. The other often changes balance sheets.

Summary: The danger is not that every climate policy is secretly identical. The danger is that fragmented rules, registries, taxes, and offset frameworks can converge into a durable architecture of control without ever announcing itself as one.

That is why the phrase “crap and trade” persists in critical circles. It captures a crude but useful suspicion: when Wall Street designs the remedy, the remedy may preserve the disease. The public should not accept atmospheric accounting as a substitute for industrial transformation.